Casualty Loss Floor

Clearing The Tax Floor On Casualty And Theft Losses Accountingweb

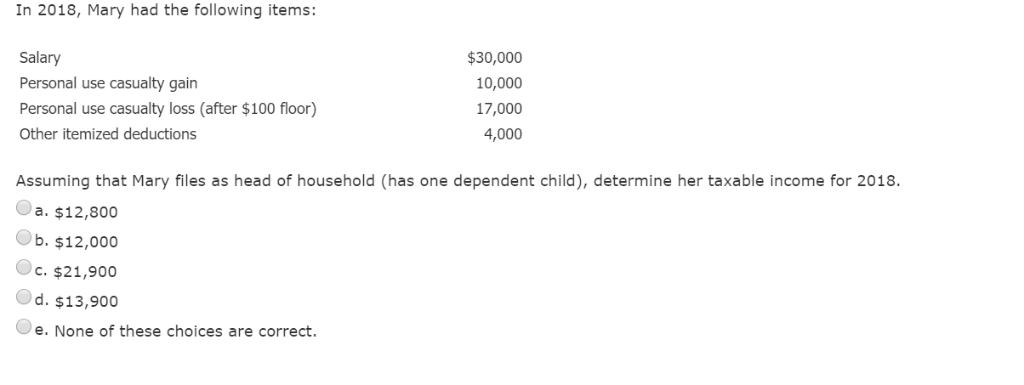

Solved In 2018 Mary Had The Following Items Salary Pers Chegg Com

How To Calculate Fair Market Value Of Property Millionacres

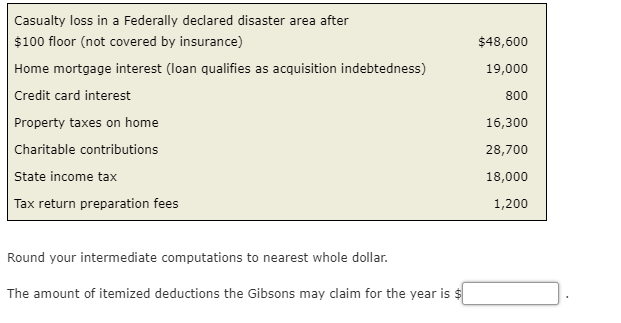

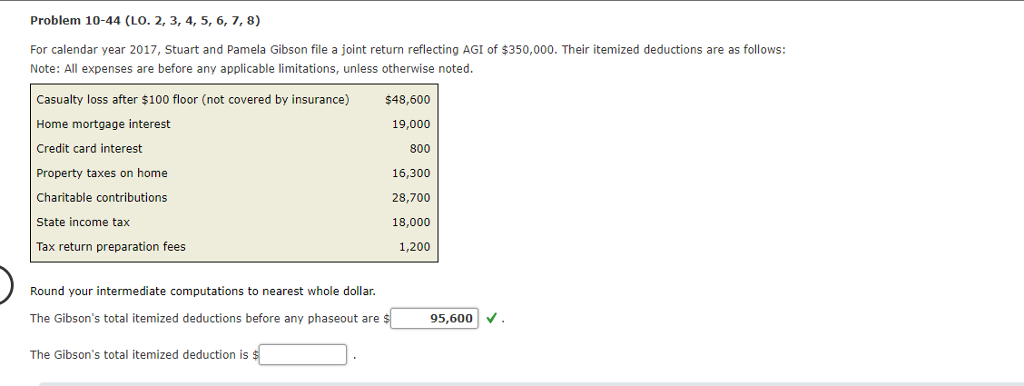

Solved For Calendar Year 2018 Stuart And Pamela Gibson F Chegg Com

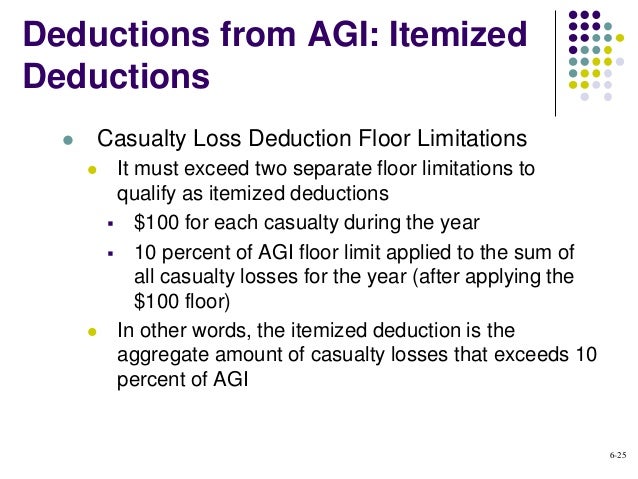

Acct321 Chapter 06

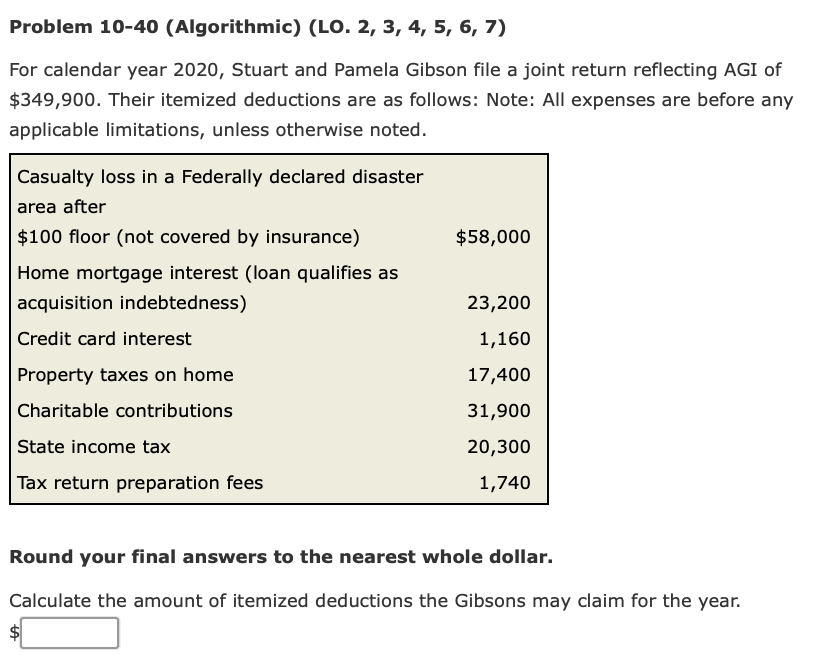

Solved Problem 10 40 Algorithmic Lo 2 3 4 5 6 7 Chegg Com

Form 4684 is used to report both business and personal losses.

Casualty loss floor.

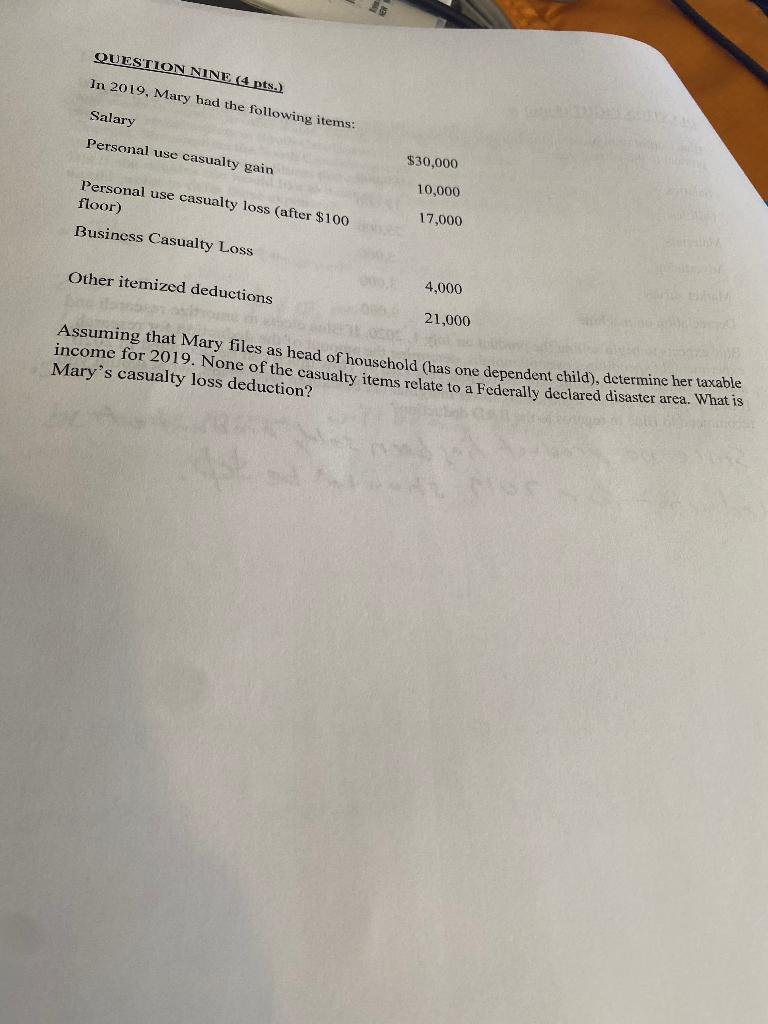

Solved Question Nine 4 Pts In 2019 Mary Had The Follo Chegg Com

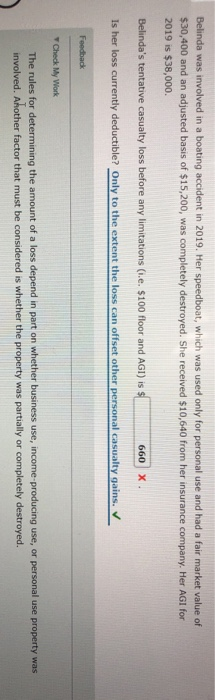

Solved Belinda Was Involved In A Boating Accident In 2019 Chegg Com

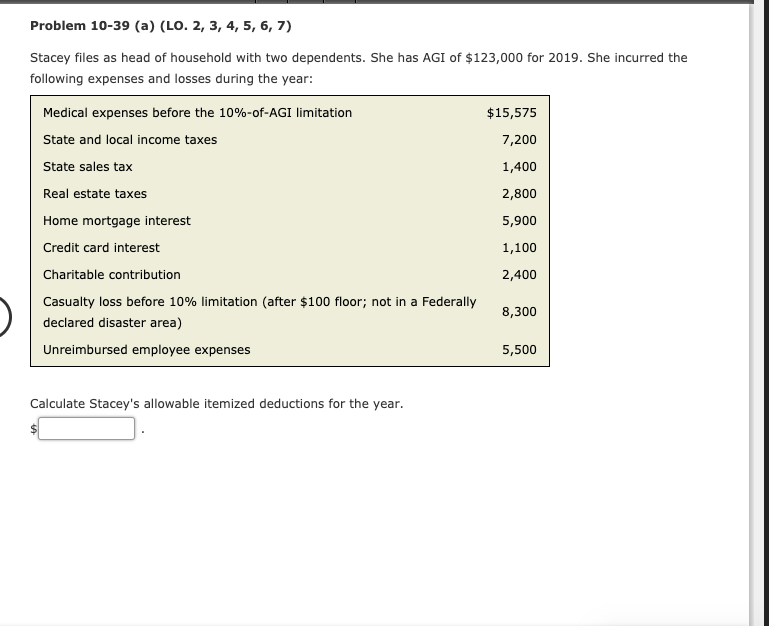

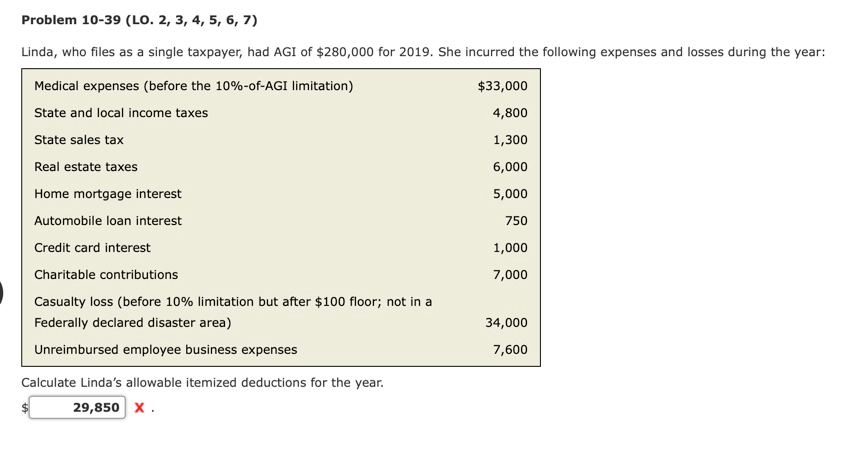

Solved Problem 10 39 A Lo 2 3 4 5 6 7 Stacey Fi Chegg Com

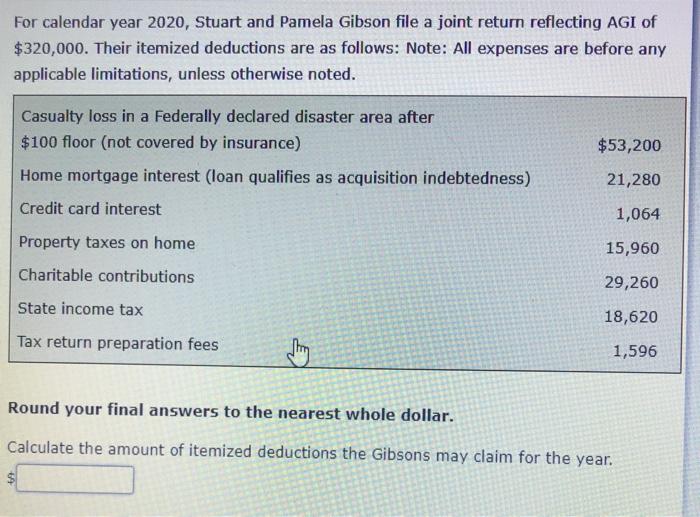

Solved For Calendar Year 2020 Stuart And Pamela Gibson F Chegg Com

Casualty Losses And Expenditures Under Sec 162 Or 165

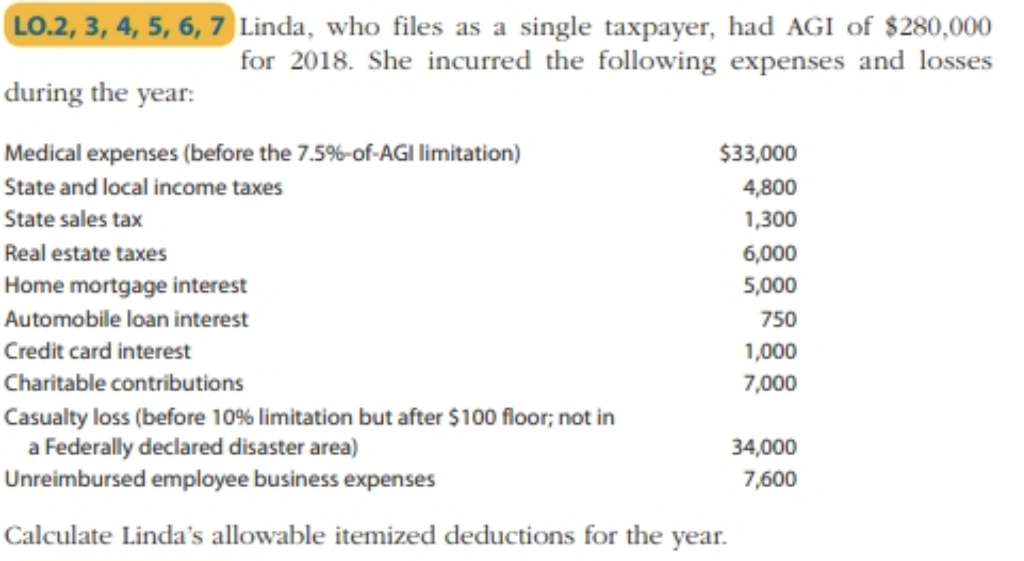

Solved Lo 2 3 4 5 6 7 Linda Who Files As A Single T Chegg Com

Solved Problem 10 44 Lo 2 3 4 5 6 7 8 For Calendar Chegg Com

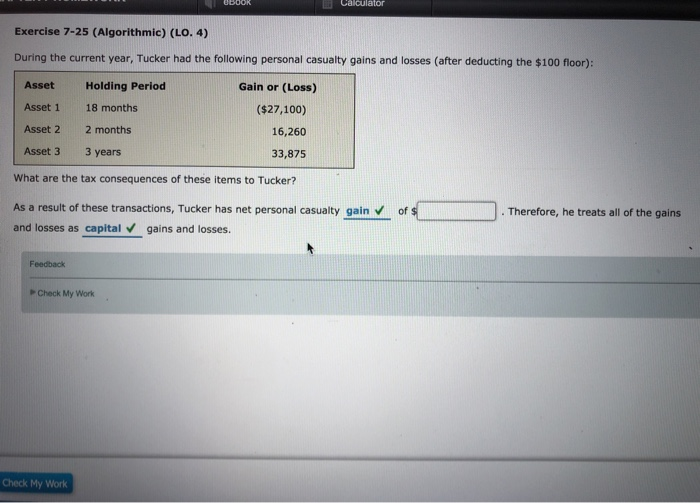

Solved Calculator Exercise 7 25 Algorithmic Lo 4 Duri Chegg Com

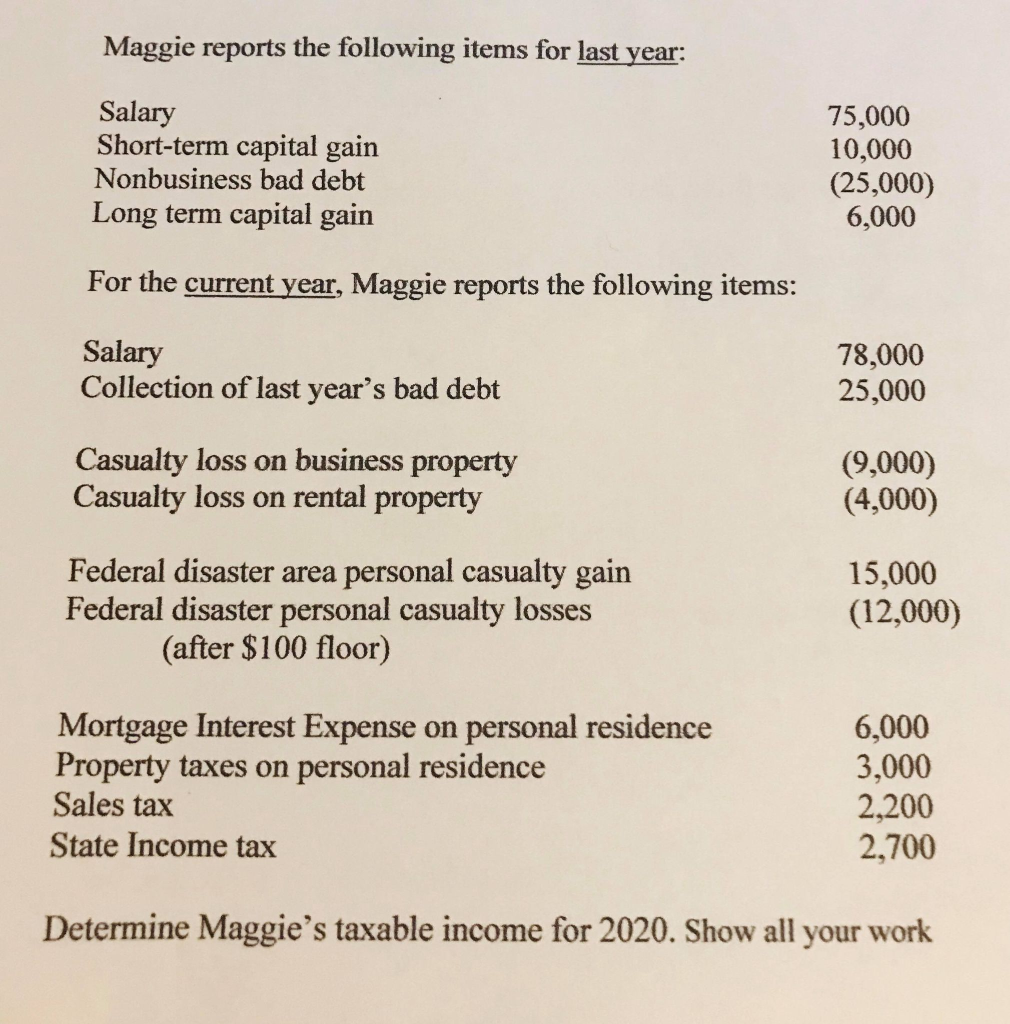

Solved Maggie Reports The Following Items For Last Year Chegg Com

Acct 421 Chapter 9 Flashcards Quizlet

Casualty Loss Deductions And Other Hurricane Related Tax Benefits The Cpa Journal

Property Loss Damage Calgary Insurance Defence Lawyers

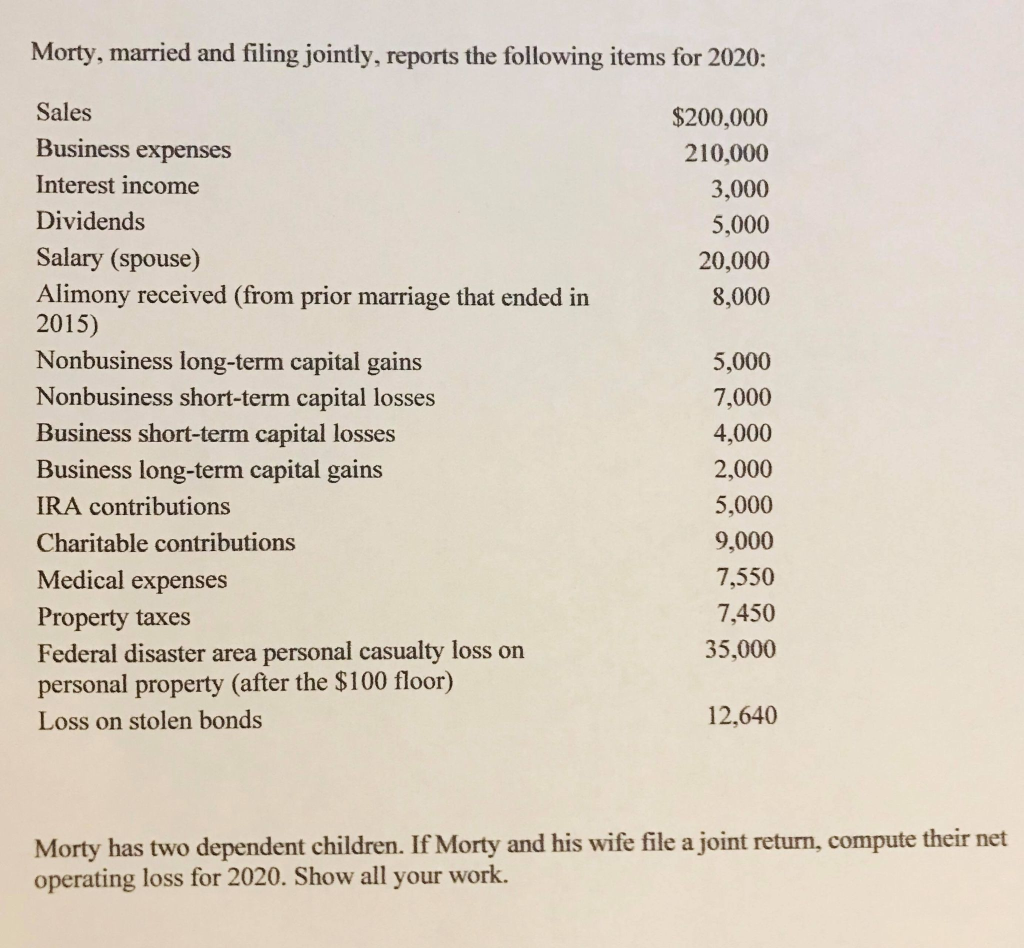

Solved Morty Married And Filing Jointly Reports The Fol Chegg Com

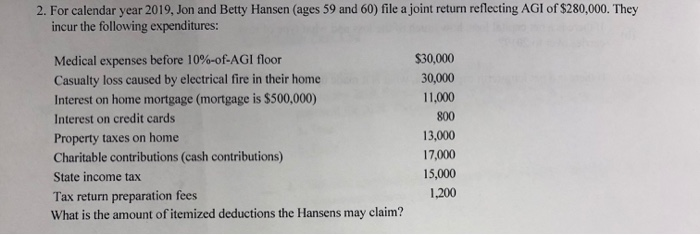

Solved 2 For Calendar Year 2019 Jon And Betty Hansen A Chegg Com

Solved Problem 10 39 Lo 2 3 4 5 6 7 Linda Who Fi Chegg Com

Factor Assessment Of Marine Casualties Caused By Total Loss Sciencedirect

Disaster Area Losses Tax Advisory Services

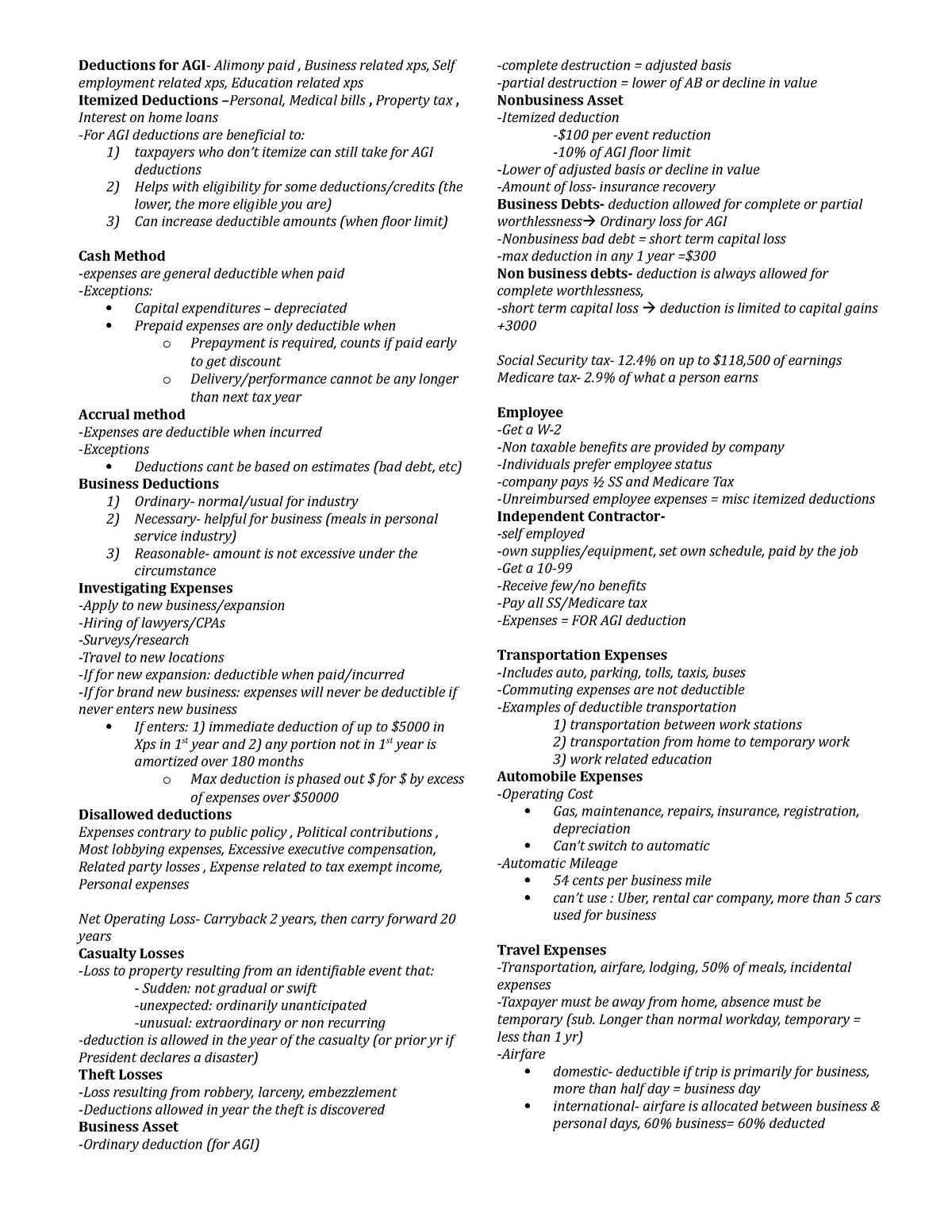

Exam 2 Cheat Sheet Summary Tax Accounting 1 Studocu

Tax And Financial Aspects Of Casualty And Disaster Losses Under The Tax Cuts And Jobs Act The Cpa Journal

Source : pinterest.com