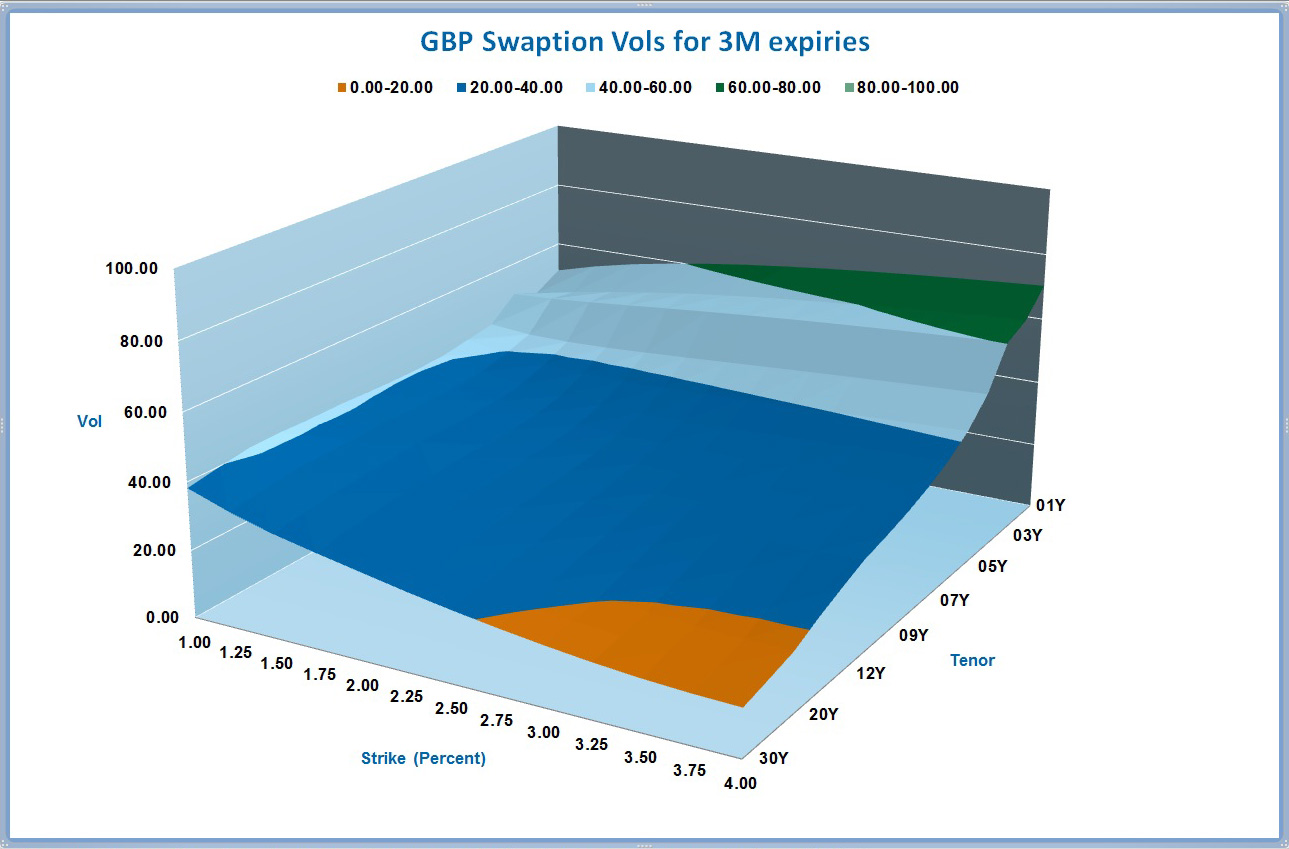

Cap Floor Volatility

Http Www Mat Ucm Es Congresos Mweek Ix Modelling Week Informes Report P1 Pdf

Interest Rate Cap Pricing Valuing Floors Financetrainingcourse Com

Http Www Mat Ucm Es Congresos Mweek Ix Modelling Week Problems Problempopular Pdf

Pin By Indiacharts On Sentiment Charts Stock Market Writing Styles Breakouts

Biotech Etfs Are At A Crucial Technical Juncture Ishares Stock Charts Nasdaq

Middle Market Debt Terms In Short Www Ennovance Com Structured Finance Investing Finance

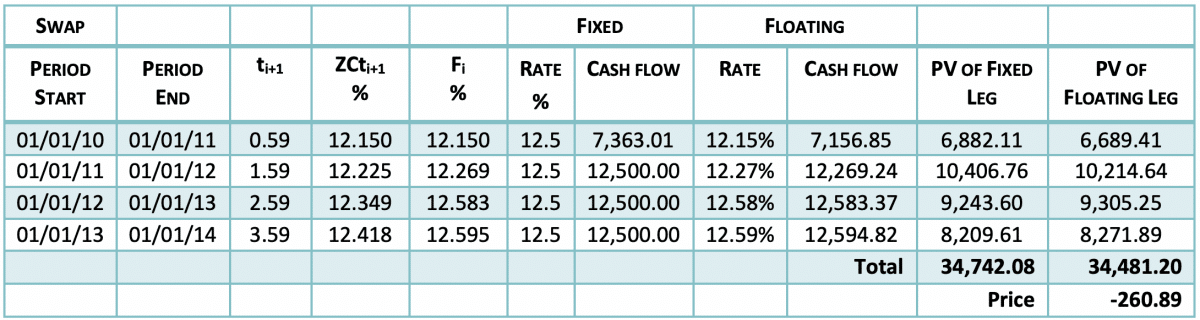

This is an iterative process to obtain caplet volatility based on cap volatility.

Cap floor volatility.

Interest Rate Amortizing Accreting Caps And Floors Valuation Finpricing

Caps And Floors Interest Rate Derivatives Coursera

5 Years Of Ethereum Proof Of Work What Did We Learn Cryptocurrency Ethereum Aanews Cryptonews Editorials In 2020 Cryptocurrency Work Proof

Interest Rate Cap Implied Volatility Surface Data Construction And Bootstrapping Finpricing

Morgan Stanley Has Some Theories For Why Hedge Funds Are Doing So Poorly Financial Markets Morgan Stanley Poor

Http Janroman Dhis Org Finance Bloomberg Capfloorcolar 20explained Pdf

Bitcoin Price Prediction Bulls Must Rally Together To Re Enter The 13 000 Zone Confluence Detector Bitcoin Price Bitcoin Crypto Coin

Interest Rate Options Global Data Tullett Prebon Information

Five Best Bitcoin Gambling Sites Gambling Sites Gambling Bitcoin

Microsoft Is Looking Hot Right Now And While I Focus On Your Next Amazing Small Cap Opportunity Greg Guenthner Is Hijacking T Tech Stocks Locker Storage Tech

How Much Are Those Dividends Costing You Meb Faber Research Stock Market And Investing Blog Stock Options Trading Stock Options Stock Market

Stanford Slac Launch Bits Watts Initiative To Create 21st Century Electric Grid The Unit Tree Swing Earth From Space

The Ultimate Guide To Indexed Universal Life Insurance Ogletree Financial

Whipsawed By Trade Fears The Dow Ends The Day Up 207 Points Regaining Lost Ground Stock Market Stock Analysis Investing

Pin On Stocks

Bitcoin Price Will Likely Increase To 5 000 Post Segwit Reasons Trends Bitcoin Price Bitcoin Blockchain Cryptocurrency

9 25 Quot Gamble Premium Vinyl Plank Flooring Vinyl Plank Flooring Gohaus Vinyl Plank Flooring Vinyl Plank Flooring

Pricing German Energiewende Products Intraday Cap Floor Futures Sciencedirect

Calibrate Hull White Tree Using Caps Matlab Hwcalbycap

Source : pinterest.com