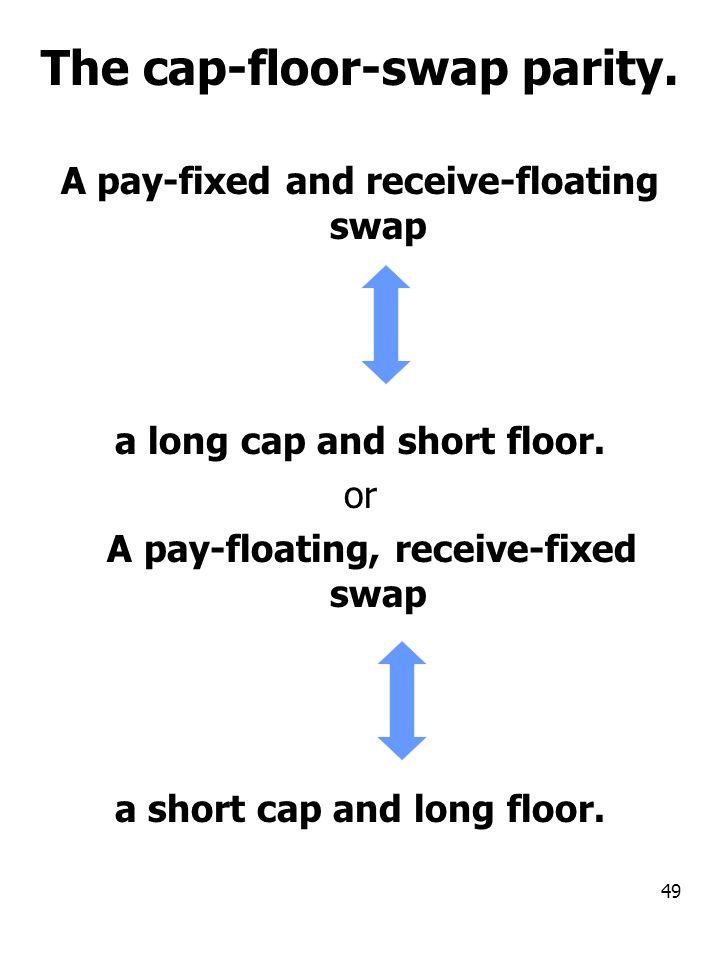

Cap Floor Parity

Interest Rate Cap Pricing Valuing Floors Financetrainingcourse Com

Financial Risk Management Of Insurance Enterprises Interest Rate Caps Floors Ppt Download

Http Janroman Dhis Org Stud Ii2008 Caps And Floors Pdf

Derivatives Relationships Long Ir Calls Short Ir Puts Please Help Me Make Connections Cfa Level Ii Analystforum

Interest Rate Derivative Pricing Ird Valuation Caps Floors And Collars Swaptions Ppt Download

Mma708 Analytical Finance Ii Exotic Cap Pricing 18 December Ppt Video Online Download

Long cap short floor gives a swap with no vol.

Cap floor parity.

Caps And Floors Interest Rate Derivatives Coursera

1 Interest Rate Options Interest Rate Options Provide The Right To Receive One Interest Rate And Pay Another An Interest Rate Call Pays Off If The Ppt Download

Advanced Risk Management I Lecture 3 Market Risk Transfer Hedging Ppt Download

Https Onlinelibrary Wiley Com Doi Pdf 10 1002 9781118818572 App4

/cdn.vox-cdn.com/uploads/chorus_image/image/61563345/Cap_In_Hand.0.png)

Salary Cramp The Illusion Of Parity In North American Sports Jewels From The Crown

Https Arxiv Org Pdf Physics 0503126

1 Fixed Income Math And Risk Measure Basic Ird Ppt Download

Chapter 3 Insurance Collars And Other Strategies Ppt Video Online Download

Pricing German Energiewende Products Intraday Cap Floor Futures Sciencedirect

What Is An Easy To Understand Explanation For Risk Parity Investment Strategy Quora

Interest Rate Caps And Floors Introduction And Valuation Youtube

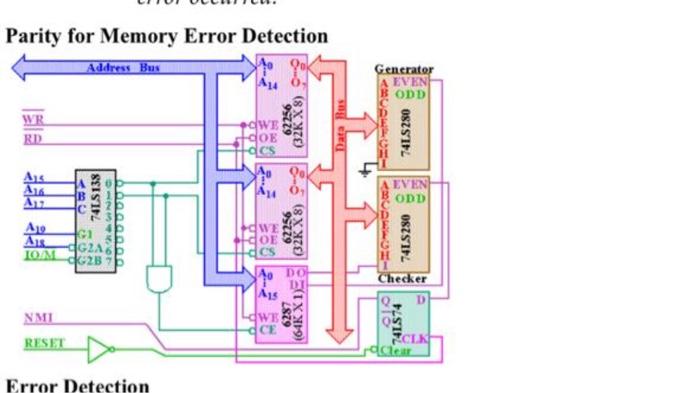

Solved 1 Determin The Address Range 2 Determine Eprom Cap Chegg Com

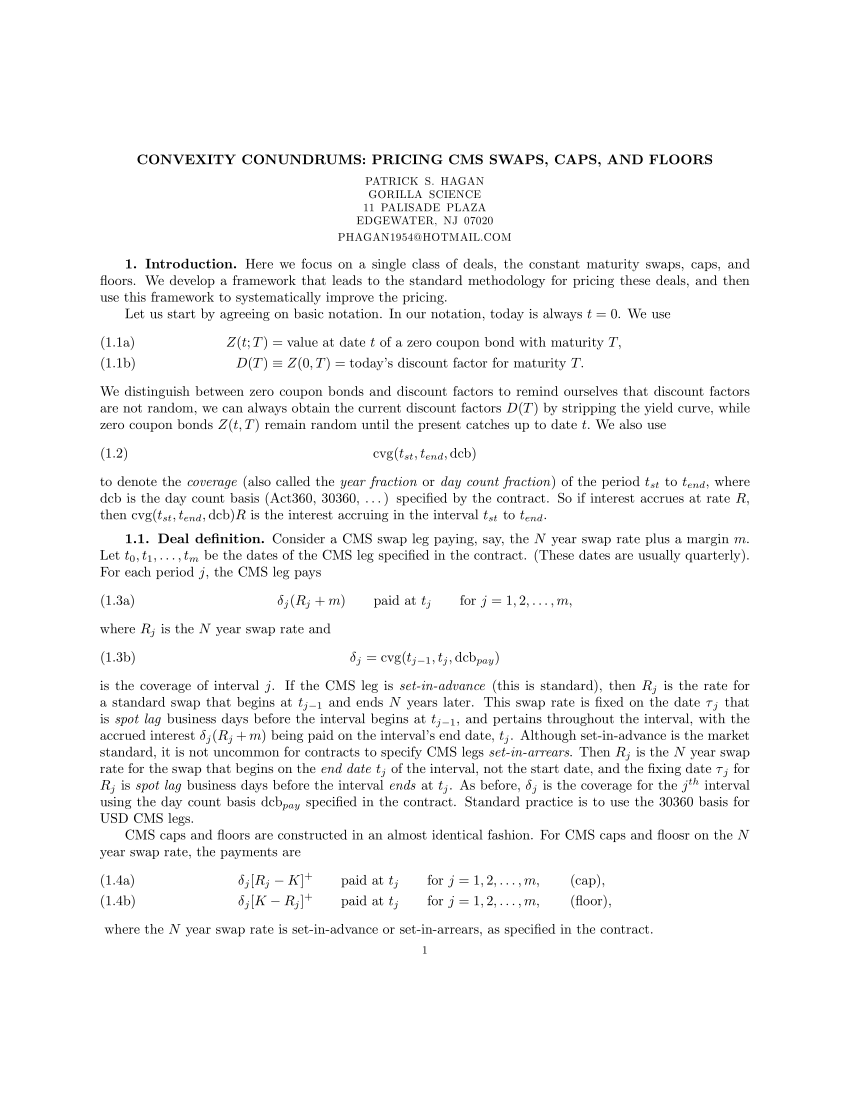

Pdf Convexity Conundrums Pricing Cms Swaps Caps And Floors

Http Homepages Ulb Ac Be Cazizieh Statf508 Files Options 20taux 20interet 20intro Pdf

Risk Parity Isn T The Problem It S The Solution Resolve Asset Management

Pdf Self Report Measures That Do Not Produce Gender Parity In Intimate Partner Violence A Multi Study Investigation

F6d5vqllst Uxm

Option Basics Financial Training Guide

Https Encrypted Tbn0 Gstatic Com Images Q Tbn And9gcrpr7boqmsycjzvszcesqr20miocbpo40ahxficaiiyjl8lbaud Usqp Cau

Source : pinterest.com